What if the insurance policy you trust to protect your high-value asset contains a hidden exclusion that leaves you responsible for thousands in repairs? Understanding exactly how auto transport insurance works is no longer a matter of simple due diligence; it's a critical component of sophisticated asset management. You likely recognize that moving a luxury or classic vehicle requires more than a standard contract. It's natural to feel a sense of unease regarding the distinction between your personal coverage and a carrier's cargo policy, particularly as federal regulations continue to evolve.

This guide provides a comprehensive analysis of the protective layers surrounding your vehicle, ensuring you possess the clarity needed to secure your investment during transit. You'll gain a complete understanding of carrier liability limits and the Federal Motor Carrier Safety Administration's new Motus filing system implemented for 2026. We will also detail the meticulous process of documenting a claim correctly, the vital role of the Bill of Lading, and how to identify when supplemental gap insurance is a necessary safeguard for your most prized automotive assets.

Key Takeaways

- Understand the evolving regulatory environment, including the Federal Motor Carrier Safety Administration’s transition to the Motus filing system and its impact on carrier compliance for 2026.

- Distinguish between the specific roles of Motor Truck Cargo and Automobile Liability coverage to gain a precise understanding of how auto transport insurance works in protecting your asset.

- Identify the significant variations in insurance ceilings between open and enclosed transport methods to ensure your luxury or classic vehicle possesses sufficient coverage.

- Recognize the Bill of Lading as a foundational legal document and learn why a meticulous pre-transport inspection is the most critical step in the claims process.

- Discover how a professional logistics partner facilitates the insurance verification process by maintaining an exclusive network of licensed and rigorously vetted carriers.

Understanding the Framework of Auto Transport Insurance

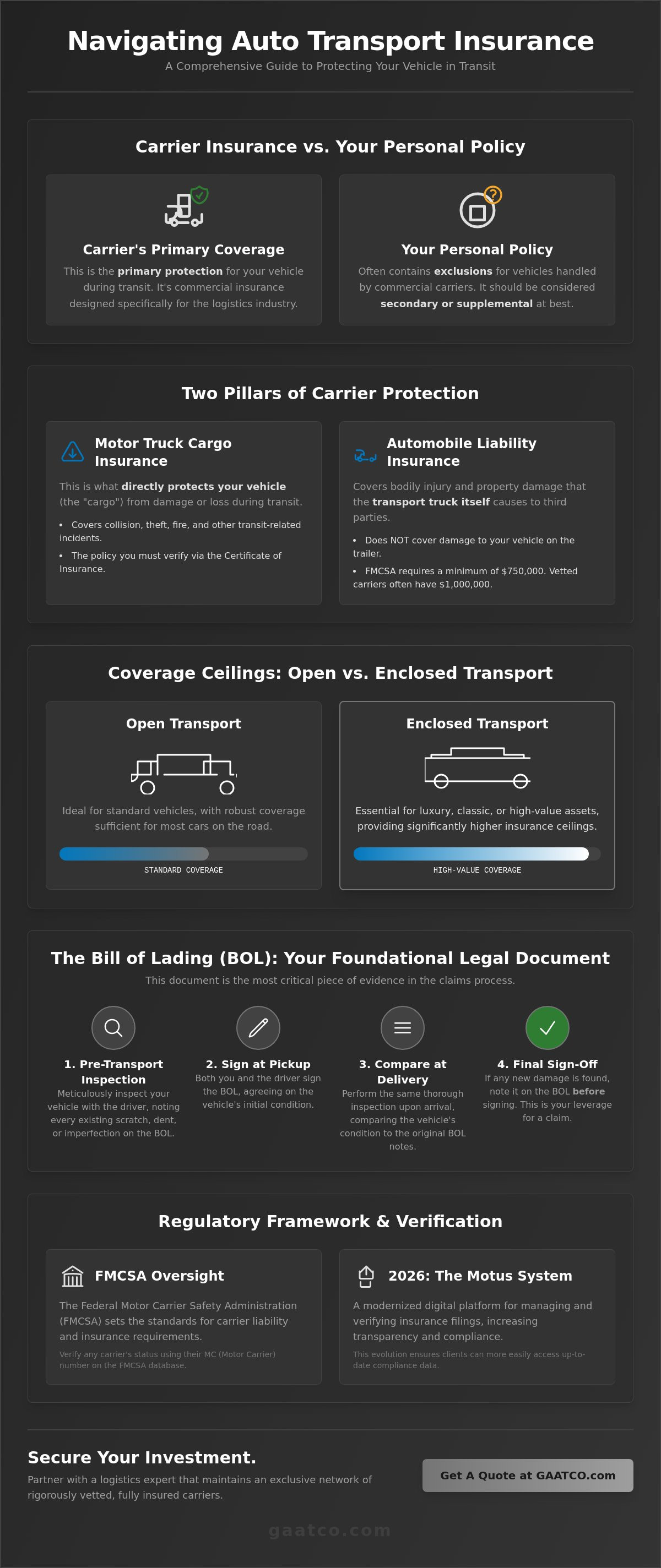

Auto transport insurance is a specialized architecture of commercial liability and cargo protection designed to shield high-value assets during transit. It's not a standard consumer policy; rather, it's a professional grade indemnity structure that addresses the unique risks inherent in the logistics industry. Understanding how auto transport insurance works requires a look at how these layers interact to provide a seamless safety net for your vehicle. Every reputable carrier must maintain a specific certificate of insurance, which serves as the primary evidence of their ability to cover potential losses during the journey.

The Federal Motor Carrier Safety Administration (FMCSA) serves as the primary regulatory body for these standards. In 2026, the industry has transitioned to the Motus system, a modernized registration platform that streamlines how insurance filings are managed and verified. This digital evolution ensures that compliance data is more transparent for clients who demand rigorous safety standards. Before any vehicle is loaded, requesting a current certificate of insurance is a non-negotiable step in verifying that the carrier possesses the financial capacity to protect your investment.

To better understand the nuances of this protective framework, watch this helpful video:

Distinguishing between a broker's financial responsibility and a carrier's cargo policy is essential for any informed shipper. While property brokers are required by the FMCSA to maintain a $75,000 bond as of January 16, 2026, this bond isn't designed to cover damage to your vehicle. It's a financial guarantee for the broker's business obligations. Actual physical protection for your asset comes from the carrier's cargo insurance, which provides the specific funds needed for repairs or replacement in the event of an incident.

The Legal Requirements for Interstate Carriers

Interstate car haulers must adhere to strict federal mandates to remain operational. The FMCSA requires a minimum of $750,000 in public liability coverage, though our network often prioritizes carriers who maintain $1,000,000 to meet higher corporate standards. This framework is anchored by the Carmack Amendment, a federal law that establishes a uniform national standard for carrier liability regarding interstate shipments. You can verify a carrier's standing by checking their MC (Motor Carrier) number through the FMCSA's official database. This verification process, combined with The Critical Role of the Bill of Lading, ensures that every aspect of the transport is legally documented and insured.

Why Personal Auto Insurance Is Not Always Sufficient

Relying solely on a personal policy during transport is often a precarious strategy. Most standard insurance providers include specific exclusions for vehicles while they're being handled by a commercial transport service. While your comprehensive coverage might offer some secondary protection if a carrier's policy is exhausted, it's rarely the primary source of recovery. Off-terminal coverage refers to a specific provision in a personal auto policy that may extend protection to your vehicle while it's in the custody of a carrier and not located at a fixed storage facility. For those seeking the highest level of security, we recommend reviewing our specialized transport services to ensure your coverage matches the value of your asset.

Primary Types of Coverage in the Shipping Process

To fully grasp how auto transport insurance works, one must distinguish between the two primary pillars of protection: Automobile Liability and Motor Truck Cargo insurance. These are not interchangeable terms. Automobile Liability addresses bodily injury or third-party property damage caused by the transport vehicle itself. In contrast, Motor Truck Cargo insurance is the specific indemnity structure designed to protect your vehicle while it is in the custody of the carrier. Federal regulations, specifically the Federal Minimum Insurance Requirements, mandate that carriers maintain specific levels of financial responsibility to operate legally across state lines.

A common point of confusion for many clients involves the application of deductibles. In a professional logistics environment, the insurance deductible is the carrier's responsibility. If a valid claim is filed, the carrier pays the initial cost, which typically ranges from $200 to $2,000, before the insurance provider settles the remaining balance. You should never be asked to pay a deductible for damage that occurred while the vehicle was under the carrier's care. For those seeking the highest level of security, exploring enclosed car transport can provide additional peace of mind by mitigating environmental risks.

Carrier Liability and Cargo Insurance Explained

Cargo insurance serves as the primary shield for your vehicle during the transit phase. Standard coverage limits vary significantly based on the equipment used. For a typical multi-car open trailer, cargo limits generally range between $100,000 and $150,000 per load. It's vital to differentiate between property damage and vehicle damage. While a policy might cover the vehicle, it may not cover damage to the trailer or loading equipment. Ensuring that the carrier's cargo limit exceeds the total value of all vehicles on the trailer is a hallmark of meticulous logistical planning.

Supplemental Coverage and Exclusions

Even the most robust policies contain specific exclusions that require careful attention. Most carrier policies do not cover "Acts of God," such as hail, floods, or unforeseen geological events. Road debris damage is another frequent exclusion for open carriers. Furthermore, personal items left inside the vehicle are almost never insured under a commercial cargo policy. If you're transporting a high-value asset that exceeds standard limits, supplemental "Gap" coverage is a wise investment. These policies, which can cost between $50 and $500 as of early 2026, provide the necessary financial bridge to ensure a high-value vehicle is fully protected against every eventuality.

Insurance Nuances: Open vs. Enclosed Transport

The choice between open and enclosed transport is not merely a logistical preference; it is a strategic financial decision that fundamentally alters the insurance profile of your shipment. While both methods provide essential protection, the insurance ceilings associated with each trailer type differ significantly. Understanding these specific limits is essential to mastering how auto transport insurance works for your particular inventory. In the professional logistics sector, the level of coverage often reflects the inherent risks and the market value of the cargo being moved.

As of early 2026, industry data indicates that open auto transport carriers typically maintain cargo insurance ranging from $100,000 to $150,000. While this is sufficient for many standard vehicles, it represents a "per load" limit rather than a "per vehicle" limit. Conversely, enclosed carriers generally provide much higher protection, with coverage typically ranging from $250,000 to $1,000,000. This disparity exists because enclosed transport is the industry standard for high-value assets that require a more robust indemnity framework.

Standard Limits for Open Carrier Shipments

Open carriers are the workhorses of the industry, often transporting between seven and ten vehicles simultaneously. It's vital to recognize that the $150,000 cargo limit is distributed across the entire trailer. If a carrier is transporting ten vehicles, the effective coverage per unit is only $15,000. This level of protection is generally adequate for standard sedans or SUVs with moderate market values. However, it leaves a significant exposure gap for late-model luxury vehicles. Shippers should always confirm the total value of the load to ensure the carrier's policy isn't over-leveraged during the journey.

High-Value Protection for Enclosed and Classic Car Transport

Luxury, antique, and exotic vehicles necessitate the superior limits found in enclosed shipping. Beyond the physical protection from road debris and weather, these trailers offer insurance riders specifically tailored for high-end assets. When you utilize GAATCO's enclosed car transport, you are accessing a network where policies are designed to cover the full appraisal value of a single vehicle rather than a shared pool. These specialized handling protocols significantly reduce the likelihood of a claim, which is why insurance providers are willing to offer such high ceilings for these specialized routes. For classic car transport, we recommend verifying that the carrier possesses an agreed-value rider, ensuring that the payout reflects the vehicle's collectible status rather than a standard depreciation model. This meticulous approach to coverage ensures that even the most rare automotive investments are handled with the quiet confidence they deserve.

The Critical Role of the Bill of Lading in Claims

The Bill of Lading is more than a simple receipt; it's the definitive legal contract between the shipper and the carrier. While previous sections detailed the layers of coverage, this document provides the actual evidence required to activate those protections. In the event of a discrepancy, the Bill of Lading serves as the primary record used by insurance adjusters to determine liability. Understanding the procedural weight of this document is a vital part of understanding how auto transport insurance works in practice. Without a correctly executed Bill of Lading, a claim is almost impossible to substantiate, regardless of the carrier’s insurance limits.

We adhere to a "Golden Rule" in the logistics industry: never sign the Bill of Lading at delivery without conducting a comprehensive inspection. Once you sign this document without noting damage, you're legally acknowledging that the vehicle was received in satisfactory condition. This signature effectively releases the carrier from further liability. For clients moving high-value assets through our specialized transport services, this documentation process is the cornerstone of a secure transit experience.

Conducting a Meticulous Pre-Transport Inspection

A successful claim begins long before the vehicle reaches its destination. You must clean the vehicle thoroughly before the driver arrives. A layer of dust or road grime can easily obscure hairline scratches or small dings, making it difficult to establish a clear baseline for the vehicle’s condition. Conduct a walk-around inspection in high-contrast lighting and take high-resolution photographs of all angles, including the roof and lower bumpers. Ensure you record the exact mileage and fluid levels on the condition report. The carrier representative must sign off on these details, providing a mutual agreement on the vehicle's state at the moment of pickup.

Documenting Delivery and Identifying Discrepancies

When your vehicle arrives, perform a second inspection that mirrors the first one. If you discover any new damage, you must note it specifically on the Bill of Lading before the driver leaves the premises. Use clear, descriptive language to identify the location and nature of the damage. Insurance providers require these "exceptions" to be documented at the time of delivery to trigger a formal claim process. While external body damage must be noted immediately, most carriers allow a 24 to 48 hour window for reporting hidden mechanical issues that weren't apparent during the initial offloading. To ensure your vehicle is handled by professionals who respect this meticulous process, you can request a shipping quote from our expert team today.

Navigating Logistics with GAATCO’s Insured Network

Choosing a logistics partner is an exercise in risk management. While the technical details of how auto transport insurance works provide a necessary foundation, the practical application of those protections depends entirely on the integrity of the carrier network. We act as a dedicated bridge between your high-stakes requirements and the complex operational realities of the transport industry. By serving as your discreet professional advisor, our team handles the intricate details of insurance verification so you can focus on the arrival of your asset.

With a 20-year history of providing reliable Door-to-Door Auto Shipping across the United States, we've refined a service model that prioritizes safety and transparency. We don't merely facilitate a transaction; we curate a secure journey. Our professionals understand that for affluent and corporate clients, the value of the vehicle often exceeds standard industry coverage, necessitating a more sophisticated approach to logistical planning and claim management.

Our Rigorous Carrier Vetting Process

Our commitment to your asset starts with a comprehensive audit of every carrier in our network. We verify that each partner maintains active status within the FMCSA’s Motus system and possesses cargo limits that align with the specific value of your shipment. This vetting process is continuous, ensuring that carriers operating in major hubs like Houston, Dallas, and San Diego meet our non-negotiable standards for reliability. This meticulous attention to detail provides a level of peace of mind that generic brokers cannot offer. By maintaining these elite partnerships, we ensure that the professionals handling your vehicle are as invested in its safety as you are.

Requesting a Transparent Shipping Quote

A professional transport experience begins with absolute clarity regarding costs and coverage. Every GAATCO quote is structured to reflect the comprehensive nature of our services, including the high-grade insurance protections discussed throughout this guide. We eliminate the anxiety of hidden exclusions by providing a hierarchical breakdown of the transport process. You'll receive professional guidance from a team that's calm under pressure and meticulously attentive to the nuances of high-end service. To begin your journey with a partner that understands the critical urgency of specialized transport, Request your customized auto transport quote today. We're ready to demonstrate the stability and expertise that decades of experience bring to your logistical needs.

Securing Your Investment for the Journey Ahead

We've analyzed the multi-layered nature of vehicle protection, from the FMCSA's Motus filing system to the critical documentation requirements of the Bill of Lading. A comprehensive grasp of how auto transport insurance works empowers you to make informed decisions regarding enclosed transport for high-value assets versus the standard limits of open carriers. It's not just about moving a vehicle; it's about safeguarding a significant financial investment through every mile of its journey.

With over 20 years of industry expertise, our team provides a bridge between your logistical needs and a rigorously vetted, licensed, and insured carrier network. We specialize in the meticulous handling of luxury and classic vehicles, ensuring that every operational detail is managed with the quiet confidence your inventory deserves. Entrusting your vehicle to a seasoned advisor allows you to enjoy the peace of mind that comes from true professional oversight. Secure your vehicle’s journey with a professional GAATCO quote and experience a standard of service that prioritizes your asset's safety above all else.

Frequently Asked Questions

Does my personal car insurance cover my vehicle during transport?

Standard personal auto insurance policies typically include specific exclusions for vehicles while they are in the custody of a commercial carrier. While some premium comprehensive plans might offer secondary protection, the carrier's cargo policy serves as the primary source of recovery during transit. We recommend contacting your insurance advisor to determine if your specific policy provides any "off-terminal" coverage for the duration of the journey.

What is the difference between a broker’s bond and carrier cargo insurance?

A broker's bond is a financial guarantee for their business operations, whereas carrier cargo insurance provides direct physical protection for your vehicle. As of January 2026, the FMCSA mandates a $75,000 bond for brokers to ensure they meet their contractual and financial obligations. In contrast, cargo insurance covers the actual repair or replacement costs of your asset if damage occurs while it is on the trailer.

What should I do if I find damage on my vehicle after delivery?

If you discover damage, you must document the discrepancies on the Bill of Lading immediately before the driver leaves the premises. Take high-resolution photographs of the affected areas from multiple angles to serve as contemporary evidence. This documentation is the essential first step in the claims process; you should then promptly notify your logistics coordinator to initiate a formal review of the incident.

Is there a deductible I have to pay if the carrier damages my car?

You aren't responsible for paying a deductible when a carrier's policy is triggered by damage they caused. The carrier is legally obligated to cover their own insurance deductible, which generally ranges from $200 to $2,000 as of early 2026. Understanding how auto transport insurance works ensures you're never pressured into paying out-of-pocket costs that are strictly the carrier's professional responsibility.

Are personal items inside the car covered by auto transport insurance?

Commercial cargo policies specifically exclude personal belongings or household goods left inside the vehicle. Transporting personal items also risks significant fines from the Department of Transportation and can cause the trailer to exceed its legal weight limits. We advise all clients to remove non-permanent fixtures and personal property before the vehicle is loaded to ensure a seamless and compliant transport process.

How do I verify if a car shipping company is actually insured?

You can verify a company's insurance status by searching their MC number through the FMCSA's Motus registration system. This modernized database provides real-time information regarding active insurance filings and federal safety ratings. Additionally, any reputable firm will provide a current Certificate of Insurance upon request, allowing you to confirm that their coverage limits meet the specific requirements of your automotive investment.

What is a Bill of Lading and why is it important for insurance?

The Bill of Lading serves as the foundational legal contract and condition report for your shipment. It's the primary document insurance adjusters use to verify the vehicle's state at both the origin and the destination. By recording every existing scratch or dent before transport begins, it provides the indisputable evidence necessary to substantiate a claim and ensures a professional resolution if new damage is identified.

Does insurance cover damage caused by weather or road debris?

Standard open carrier insurance policies often exclude damage resulting from "Acts of God," such as hail or floods, and may not cover minor road debris. This is a primary reason why we recommend enclosed transport for high-value or classic vehicles. Enclosed trailers offer a physical barrier against environmental hazards and typically carry much higher insurance ceilings to cover the full appraisal value of specialized automotive assets.